Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  BNB

BNB  XRP

XRP  USDC

USDC  Solana

Solana  JUSD

JUSD  Dogecoin

Dogecoin  Figure Heloc

Figure Heloc  Cardano

Cardano  Wrapped stETH

Wrapped stETH  Bitcoin Cash

Bitcoin Cash  WhiteBIT Coin

WhiteBIT Coin  Wrapped Bitcoin

Wrapped Bitcoin  Wrapped eETH

Wrapped eETH  USDS

USDS  Binance Bridged USDT (BNB Smart Chain)

Binance Bridged USDT (BNB Smart Chain)  LEO Token

LEO Token  Coinbase Wrapped BTC

Coinbase Wrapped BTC  WETH

WETH  Stellar

Stellar  Ethena USDe

Ethena USDe  Zcash

Zcash  Hyperliquid

Hyperliquid  Canton

Canton  Sui

Sui  Litecoin

Litecoin  Avalanche

Avalanche  USD1

USD1  USDT0

USDT0  Hedera

Hedera  Shiba Inu

Shiba Inu  World Liberty Financial

World Liberty Financial  sUSDS

sUSDS  Ethena Staked USDe

Ethena Staked USDe  Toncoin

Toncoin  Polkadot

Polkadot  MemeCore

MemeCore

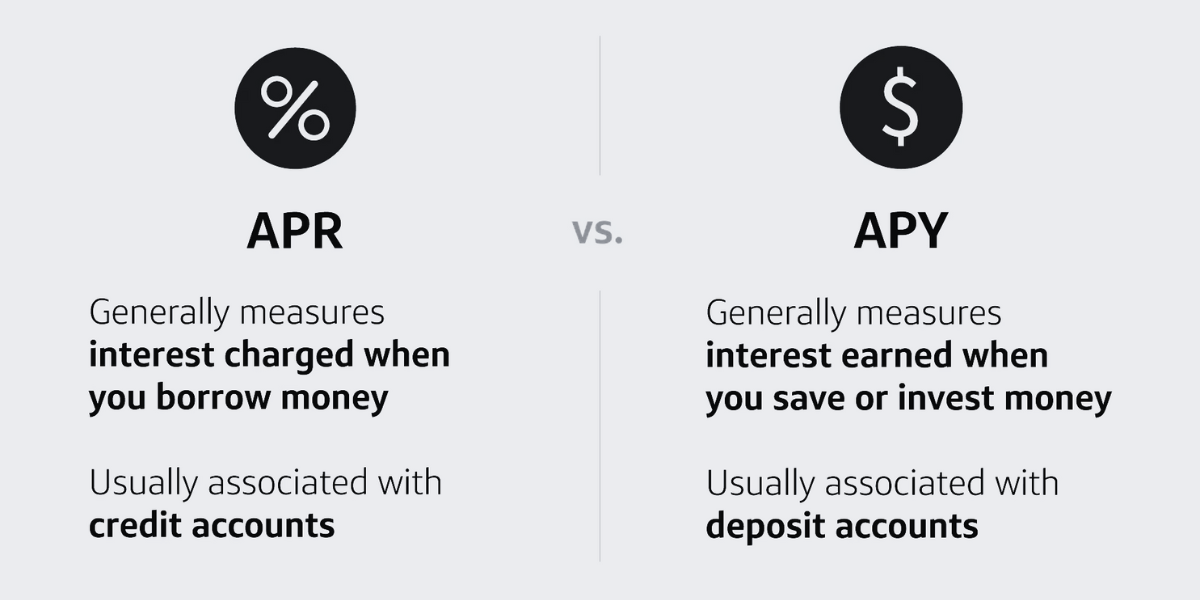

APR and APY might look quite similar, but they measure different things. Knowing what they mean can help you make better financial choices, especially in the context of cryptocurrency.

What is APR?

APR, or Annual Percentage Rate, is the amount it costs to borrow money over a year. In crypto, it’s commonly used for loans or staking rewards. It’s just the interest rate alone, but it doesn’t factor compounding into APR.

For instance, if you borrow a crypto loan of $1,000 with a 10% APR, you will have to pay $100 in interest after one year. That is without additional fees or compounding.

In DeFi, APR often gets applied to borrowing or lending tokens. If you’re lending out stablecoin with an APR of 5%, in a year’s time, that’s 5% of principal. But remember, APR does not consider how often you get paid or how reinvesting those payments can grow your returns.

What affects your APR?

Many things can determine your APR, for example:

- Credit Score: If you have a good credit score, you’ll get a low APR, but if you have a bad credit score, you might get a high APR.

- Loan Type: Various loans carry different APRs. For instance, a mortgage will have a lower APR compared to a credit card.

- Lender: For the same type of loan, various banks or lenders may provide different APRs.

- Loan amount and term: The amount you borrow and how long you take to repay it can change the APR. So, shorter loans may have lower APRs.

- Market Rates: If interest rates in the economy increase, your APR may increase.

- Down Payment: The more significant the down payment, the better the APR given by the lender.

APR vs. Interest rate

APR and interest rates are similar but not the same. The interest rate is the base rate, while APR includes fees. For example, if you take a crypto loan with a 5% interest rate and a 2% platform fee, the APR becomes 7%. APR helps borrowers understand the total cost of borrowing.

What is APY?

APY, or Annual Percentage Yield, will measure how much you earn on your savings or investment, with the compounding interest. Compounding occurs when the interest you are earning is added to your original amount and then that total earns interest on it. In crypto, compounding may happen daily, weekly, or monthly depending on a given platform.

For example, if you deposited $1,000 in cryptocurrency into a savings account with a 5% APY, compounded monthly, you’ll earn a bit above $50 for a year. This is because every month, your earnings are added to your balance, raising the amount that future interest gets computed on.

APY vs. interest rate

The interest rate only reflects the simple annual return, whereas APY takes into account compounding. For instance, a 10% APY with monthly compounding will be slightly higher than a 10% annual interest rate. That is why APY is more useful for understanding actual returns.

APR vs. APY: What is the difference?

| APR (Annual Percentage Rate) | APY (Annual Percentage Yield) | |

| Definition | Measures the annual cost of borrowing or return on investment, excluding compounding | Measures the annual return on investment, including compounding |

| Compounding | No | Yes |

| Usage in Crypto | Loans and staking rewards | Yield farming, staking, and savings. |

| Calculation | Simple interest over a year | Compound interest over a year, considering the frequency of compounding |

| Impact on Costs/Returns | Straightforward estimate of costs or returns | More accurate representation of returns with compounding |

| Example (Borrowing) | Borrow $1,000 at 10% APR, and pay $100 in interest in one year | Borrow $1,000 at 10% APY, and pay slightly more due to compounding |

| Example (Saving) | Stake $1,000 at 10% APR, and earn $100 in one year | Stake $1,000 at 10% APY, and earn slightly more due to compounding |

| Relevance | Better for understanding borrowing costs | Better for understanding investment growth |

Example

Here’s an example to understand the difference between APR and APY:

- Borrowing: If you take a $1,000 crypto loan at a 12% APR, you’ll owe $120 in interest after a year. However, if compounding is applied monthly, and the rate is expressed as APY, your total cost could be closer to $126.

- Saving: If you deposit $5,000 in a staking pool offering a 12% APY with monthly compounding, your returns will exceed $600 due to the added effect of compounding.

The Borrower’s Perspective

The annual percentage rate (APR) is the most important figure to pay attention to when borrowing. It’s the figure that lets you see what the average baseline cost of a loan is. For example, if you borrowed 5,000 USD in stablecoins at an APR of 12%, you know that, assuming there isn’t compounding, you’ll have $600 in interest owed after one year.

However, borrowing in crypto is not that simple. Although APR gives a simple picture, many platforms apply compounding, which makes the actual cost higher than the quoted APR. In such cases, the effective interest rate is more similar to the APY. Borrowers need to carefully look at loan agreements for terms like “compounding frequency” or “effective rate” to avoid surprises.

Additionally, crypto lending markets are influenced by the volatility and liquidity of the assets involved. If you are borrowing highly volatile cryptocurrencies, the platform may adjust rates dynamically. APR in such scenarios might shift, leading to variable borrowing costs. Borrowers need to monitor these changes and plan repayments accordingly to avoid higher-than-expected costs.

There are also platform-specific fees that can greatly add to the APR. The APRs on some decentralized finance platforms include these fees, while on others, they appear separately. The difference makes comparison across platforms difficult but is necessary for an accurate cost of borrowing estimate.

The Saver’s Perspective

Annual percentage yield (APY) is much more relevant to the saver or investor, as it indicates how much more your money will grow with account compound interest. This aspect is especially crucial for cryptocurrency, because staking, yield farming, or liquidity provision usually involves relatively frequent compounding. The greater the compounding frequency, the higher the actual returns would be.

For instance, if you are staking $10,000 in a DeFi pool with an APY of 10% that compounds daily, your returns would be more than the simple $1,000 that a 10% APR would give you. Instead, your compounded returns could grow to $1,051 or more, depending on the compounding frequency. In longer periods, this difference is even more apparent, making APY a better indicator of real growth.

The compounding frequency, platform reliability, and stability of the tokens should be at the forefront when comparing APYs for savers. Platforms that compound daily or weekly tend to give better returns compared to those that compound monthly or annually.

APR vs. APY: Which is better?

Neither APR nor APY is inherently better; it depends on your goal. If you’re borrowing, focus on the APR to understand the base cost. If you’re saving or investing, look at the APY to see how much your money can grow with compounding.

Some liquidity pairs offer huge yields in decentralized exchanges (DEX), especially in meme coins, because of:

- Liquidity and Slippage: New or less popular pairs may offer higher yields to attract liquidity providers and reduce slippage.

- Scarcity: Limited token supply can increase demand, leading to better yields for liquidity providers.

For example, if you’re lending out a stablecoin on a DeFi platform, an APY of 8% with daily compounding will yield more than an APR of 8%. But if you’re taking a loan, a lower APR is more favorable as it means less interest to pay.

Cryptocurrency protocols also use APR and APY in many ways. For instance:

- Liquidity Pools in DEXs: Platforms like Raydium, Uniswap, and Sushiswap reward liquidity providers with APR. The rewards often include transaction fees and bonus tokens.

- Staking in CEXs: Centralized exchanges like Binance show staking rewards in APR. However, you can enable auto-savings on Binance, where your rewards are automatically added to your balance, effectively turning APR into APY.

In DEX like Raydium, adding liquidity in Memecoin pairs can be beneficial from incredibly high APR, but high risk in return

Conclusion

In a nutshell, understanding the difference between APR and APY is crucial. APR is ideal for estimating borrowing costs, while APY is better for understanding investment growth. Both metrics are essential for making informed financial decisions. Always compare these rates carefully, read the terms, and choose what aligns with your financial goals.

FAQs

Is it better to earn APR or APY?

It’s generally better to earn APY than APR if you want to grow your money. APY includes the effect of compound interest, which means you earn interest on both the money you deposit and the interest you’ve already earned. This helps your money grow faster.

The APR, on the other hand only indicates how much interest you pay or earn that does not count on compound interest. So if you are saving money, APY is usually better because it will give you a higher return over time.

What is a good APR rate?

A good APR rate depends on what you are borrowing for. If it’s a credit card, then a good APR is usually 15% to 20%, but some people can get lower APRs if they have excellent credit scores.

Mortgages have good APRs under 4% to 5%. Crypto lending APRs are around 10%. The lower the APR, the lesser interest you will pay overtime. Always shop around and compare what rates are from which lenders to get a good deal.

What is 5% APY in APR?

To convert 5% APY into APR, first understand the meaning of compounding in APY and the lack of compounding in APR. 5% APY is nearly equivalent to around 4.88% APR, as calculated based on compounding interest frequencies.

This is because the more often interest is compounded, the higher the APY will be compared to the APR. You can use the formula to figure out the true APR, but, in general, for the same rate, APY will be higher than APR.

Can APR and APY rates change?

Yes, the APR and APY rates may differ. Your APR will vary based on whether your lender offering a variable-rate loan or your interest rate increases or lowers with market changes.

Your APY may also vary if the bank changes the interest rate offered, or if they change how often they compound interest. It’s important to check your rates regularly to see if they have changed and to make sure you’re still getting a good deal.

What’s the difference between an interest rate and APY on a CD?

The interest rate on a CD (Certificate of Deposit) shows how much you will earn in interest over the year, but it doesn’t include the effect of compounding. Instead, APY shows how much you will make in one year if the interest is compounded, meaning you earn interest on both your deposit and the interest added.

So, APY refers to a clearer picture of how much your investment will grow. If your CD compounds interest more frequently, the APY will be higher than the interest rate.

The post APR vs. APY: What’s the Difference? appeared first on NFT Evening.